TriniTuner.com | Latest Event:

Moderator: 3ne2nr Mods

Redman wrote:

On another not are we allowed to critique other posts that are IMHO posting questionable info?

Why pay fees and commissions to a Third Party from your hard-earned monies that are being invested ?

Premera wrote:AllTrac wrote:i have group life and group medical offered to me by my job with guardian life, i also have maritime admed, so im pretty set wrt to critical illness.

How about posting some info here on what retirement or investment policies you all offer so we can all discuss it and critique it.

No probs.....

At Guardian we have registered and unregistered annuities :

Registered Annuities pros & cons :

pros - tax break on contributions made

long term investment so positive performance is pretty much guaranteed

Registered with BIR so funds are insured.

1% minimum guaranteed rate ( some competitors offer ZERO )

cons :

Not registered with BIR so no tax break

25% charge if policy is surrendered before maturity

No access to funds, unless surrendered or matured.

Charges on payments made for the first few years

UNREGISTERED ANNUITY

pros - not registered with government so no taxes on monies

again, long term product so good performance is pretty much guaranteed.

Conservative, Moderate and Aggresive funds to choose from when investing ( can split premiums in all three funds and switch as seen fit )

No penalties for surrendering after 5 years

Access to monies before maturity ( after 5 years )

Cons - no tax break since not registered with BIR

No minimum guarantee rate.

Penalties if surrendered within first 5 years

We also have an investor portfolio attached to our Life Evolution product. Same concept as an annuity except, no penalties at all for withdrawals, no minimum guaranteed rate, no charges at maturity ( 65 or older if you choose ), full access to 100% of funds, no tax break as not a registered pension product. Pretty good performance over the past year, over 6% growth, despite economic downturn

I can email you guys our monthly growth statistics and information on our other products, its too much to post here.

Trac, one question for you ? What formula was used by the Agent to calculate how much Life and CI coverage is sufficient for you ? The reason i ask is because, out of every 5 persons i meet, 3 of them are vastly under-insured and are unaware till the calculations are done for them.

Feel free to pm me your address ok.

Information and analysis is FREE

AllTrac wrote:Redman wrote:

On another not are we allowed to critique other posts that are IMHO posting questionable info?

please do, thats one of the many purpose of this thread, more geared towards the investor, so all info, pros and cons is gladly invited, just no name calling and mud slinging we can keep it civil, no policy is perfect so im sure there will be a catch some where or some holes, i expect that, its is the size of those loopholes that concerns me hence this thread.

My reason for dropping the maritime rumor in this thread was so find out if there is any truth to it as my family current have policies with them and im about to take one out, but since that rumor im questioning the stability of the company. One this the outshined most of the other policies is that admed pays instantly and does not require a 30 day survival after diagnosis to pay up.

Premera wrote:thanks for the big up c.chiney.

redman, with respect to interest rates ( high or low ), the point i'm trying to make is that the moment one changes the focus of the goal intended through the product purchased then it will always be a run around for them, always looking for a better rate of return.

In my experience in the Industry, 5-7 years aback, I had clients that went to CLICO for the 15% rate offered and so on, 3-4 years ago when the clico collapse occurred the cried blood as they came to me asking " can you help me get back our money "

These client's had millions invested and even those that has under 500k were frustrated.

Note that at the same time, Guardian was offering between 9-11% rate of return, with a minimum guarantee on the policy and yet they opted to run down the high interest rate.

The clients were guilty of jumping in at clico with eyes closed because they assumed that there was a minimum guarantee on the clico policy as well. Imagine their surprise when the collapse came.

After the collapse, the mindset of the investor has changed from securing high interest to securing their capital. I have clients that say interest is third priority for them.

1st - Capital Guarantee / Preservation

2nd - Access to funds

3rd - Stability of company / investment fund

The CLICO demise has in my opinion made us all wiser in that we seek detailed information before making decisions, rather than just going by what the agent tells us. We educate ourselves as best as we can regarding anything we do with our monies.

My take on interest is it should NOT be the #1 priority when investing. Stability, fees, penalties, access to funds should be the top list priorities.

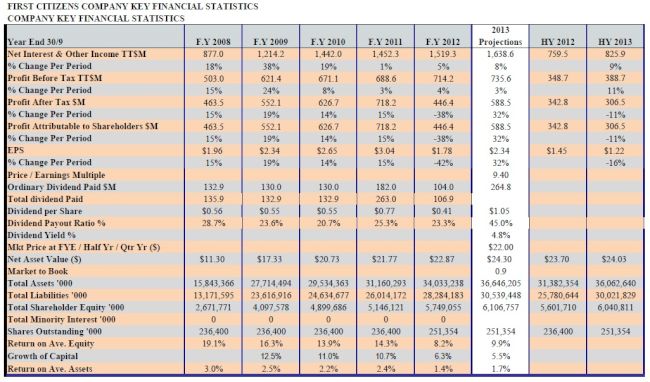

DVSTT wrote:FCB shares, yes or no?

pugboy wrote:I been using WISE over 15yrs.

Stocks are a fairly decent investment,

I usually buy some once a year, usually at the start.

Some good stocks for me have been Neal/Massy, Republic, RBTT and lately Witco.

Busts have been TCL and Guardian Insurance.

Unilever and Witco were outstanding last year.

After you build up a critical mass the dividend checks are a good paycheck every quarter instead of the pittance you get from UTC.

Some stocks have gone up a bit so far for the new year.RapToR wrote:anyone knows a good stock broker ?

PapaC wrote:DVSTT wrote:FCB shares, yes or no?

Love to hear some intelligent fedback on this.

Been reading up on it,, but not all to familiar with the jargon.

This seems like a good investment IMHO.

Return to “Ole talk and more Ole talk”

Users browsing this forum: Duane 3NE 2NR, redmanjp and 101 guests